In This Age of Plenty by Louis Even

Preface to the 1946 French Edition

This book deals with Social Credit, but in no way does it sum up the matter. In fact, Social Credit is a whole new orientation given to civilization: It deals with social and political matters as well as, or more so, with matters of economics. We even believe, as Douglas did — to whom the world owes this enlightening doctrine — that rectifying economics along Social Credit principles, is impossible without first rectifying politics.

This book deals with Social Credit, but in no way does it sum up the matter. In fact, Social Credit is a whole new orientation given to civilization: It deals with social and political matters as well as, or more so, with matters of economics. We even believe, as Douglas did — to whom the world owes this enlightening doctrine — that rectifying economics along Social Credit principles, is impossible without first rectifying politics.

In this book, however, except for a few thoughts arising from the repercussions of a flawed and dominating financial system on politics, we have confined our study to the economic objectives and monetary proposals of Social Credit.

The title of the book — In This Age of Plenty — clearly shows that we are dealing with an economy of plenty, of an easier access to the immense possibilities of modern production.

“Old economics” could well have been found under the title of “The Age of Gold” or any other rare commodity, at a time when production itself often failed. But progress is ignored and logic is set aside when, to confer claims upon an automated production, we insist on keeping an instrument linked to scarcity.

In the first part of this book, we recall essential and very simple notions that are readily admitted by everyone, but which are almost totally ignored by the present economic organism. The ends no longer direct the means. A brief study of the present monetary system shows that money governs where it ought to serve. We offer the Social Credit proposals as a remedy, giving an outline without going into the methods of implementation. The problem, we believe, lies not so much in developing an operational technique, but in getting people to agree on proposals that seem both too simple and too bold to the minds of those who are used to losing sight of the ends and to getting bogged down in the complexity of the means. Therefore, several chapters are meant to be a plea in favor of the Social Credit doctrine.

The second part is made up of reprints of speeches and articles that are likely to shed light on different aspects of Social Credit.

In offering this book to the public, we have set our sight on the average reader. Even when dealing with precise topics, we have done our best to avoid technical terms, since they are more likely to make the readers weary than to enlighten them. We have striven to write in such a way as to be readily understood by the largest number of people. This is in line with an economy of plenty at the service of all and everyone.

Montreal, May 1st, 1946.

LOUIS EVEN

Click HERE to Download the Book:

“In This Age of Plenty” by Louis Evan

“In This Age of Plenty” by Louis Even

Introduction: Social Credit: not Socialism, not a political party by Alain Pilote

Not Socialism

New students to the Social Credit philosophy should be forewarned: Social Credit is not a form of socialism. Social Credit is not a political party.

Because of the word social in Social Credit, some people take it for granted that it must be a form of socialism and therefore reject it firsthand. On the contrary, Social Credit is the best way to fight socialism and communism while protecting private property and individual freedom. A Dominican Father who studied the Social Credit proposals, went so far as to write: “And if you want neither Socialism nor Communism, bring Social Credit in array against them. It will be in your hands a powerful weapon with which to fight these enemies.”

And in 1939, a Commission of nine theologians appointed by the Bishops of Quebec found that Social Credit was not tainted with socialism or communism and was worthy of close attention. In fact, Social Credit wants every member of society to become a true capitalist, a shareholder in the wealth of the country. If the “social” in Social Credit worries some people, Douglas’s financial proposals can also be referred to by other names: Public Credit, Economic Democracy, or New Economics.

Not a political Party

As concerns political parties, it is true that parties called Social Credit have existed in the past and this explains why some people may be confused: a Social Credit party existed on the federal scene in Canada for some years, another took power in the Province of Alberta from 1935 to 1971 and another in the Province of British Columbia from 1952 to 1991 except for three years, from 1972 to 1975. Neither one of these provincial parties applied Social Credit. The very day he took office as premier, in 1952, Bennett, B.C.’s Social Credit leader, declared that his party would do absolutely nothing to apply Social Credit principles. There was actually nothing even closely related to real Social Credit in this party or its platform; it might have been more accurately called “conservative”.

The fact is, there is no need for a so called Social Credit Party to have C. H. Douglas’s Social Credit principles implemented. These principles can be applied by any political party presently in office, whatever its name — Liberal, Conservative, etc. Some people may have thought that promoting Social Credit parties was a better way to promote Social Credit, but C. H. Douglas and Louis Even thought exactly the opposite.

As they pointed out, the creation of Social Credit parties was even a nuisance, and did nothing but prevent the implementation of real Social Credit. For as soon as you use the words Social Credit to name a political party, you have closed the minds of people of other parties, preventing them to even study Social Credit, since they will consider it only as another party to be fought.

Real democracy means that elected representatives are sent to Parliament precisely to represent their constituents and to express the will of their constituents. So the point is not to create new parties, and divide the people even more, but to unite the people around common objectives and then to put pressure on the Government to implement these objectives. This method of pressure politics is the one advocated by the Michael Journal.

In a speech given to Social Crediters on March 7, 1936, Douglas said that the idea that a Social Credit party should exist (in any country) was a “profound misconception”. He even added: “If you elect a Social Credit party… it would be to elect a set of amateurs to direct a set of very competent professionals. The professionals, I may tell you, would see that the amateurs got the blame for everything that was done.”

This is precisely what happened in Alberta in the 1930s. Douglas wrote a very interesting book on that subject, entitled “The Alberta Experiment”, from which the following information is taken.

The Alberta Experiment

William Aberhart was the principal of a Calgary High School who commanded a province wide audience every Sunday with his religious broadcasts. He came across a book on Social Credit and, being so carried away by this new light, he began to use his radio program to preach the “gospel” of Social Credit, and to mobilize support for it. Hundreds of study groups soon appeared across the province, and a majority of Albertans became in favour of Social Credit. The ruling party in Alberta at the time, the United Farmers, was also open to Social Credit but insisted that it could only be applied nationwide and not provincially. Aberhart disagreed and decided to present Social Credit candidates in the 1935 provincial election. He captured 56 of the 63 seats in the provincial legislature. They were all new to politics, being a “set of amateurs” and no match for the Financiers.

For example, when Aberhart took office, instead of listening to Douglas‘s advice, he went to Ottawa to seek financial assistance. Upon his return, he was given an economic adviser, Mr. Robert Magor, who had obviously only one objective in mind: to discredit Social Credit. Measures were adopted that were just the opposite of Social Credit, what Douglas called “a policy of capitulation to orthodox finance… Almost every mistake of strategy which could be made in Alberta had been made.” William Aberhart was the principal of a Calgary High School who commanded a province wide audience every Sunday with his religious broadcasts. He came across a book on Social Credit and, being so carried away by this new light, he began to use his radio program to preach the “gospel” of Social Credit, and to mobilize support for it. Hundreds of study groups soon appeared across the province, and a majority of Albertans became in favour of Social Credit. The ruling party in Alberta at the time, the United Farmers, was also open to Social Credit but insisted that it could only be applied nationwide and not provincially. Aberhart disagreed and decided to present Social Credit candidates in the 1935 provincial election. He captured 56 of the 63 seats in the provincial legislature. They were all new to politics, being a “set of amateurs” and no match for the Financiers.

It must also be mentioned that Aberhart, although sincere enough, had also little knowledge of Social Credit. He did not understand its technical basis. This often led him, in an effort to simplify Douglas‘s ideas, to distort them. In the following years, fifteen Social Credit bills were voted on by the Alberta Government, but they were all vetoed by higher authorities. They were either disallowed by the Federal Government or ruled unconstitutional by the Supreme Court.

The main point of contention was that money and banking is under federal jurisdiction, according to the Canadian Constitution. Douglas explained to Aberhart that Alberta could bypass this difficulty by making use of its own credit by establishing a provincial credit system, since the Constitution grants to the provinces the right to “raise loans upon the sole credit of the Province.” As Douglas wrote in The Social Crediter of September 11, 1948: “When Mr. Aberhart won his first electoral victory (in 1935), all he did was to recruit an army for a war (against the monopoly of credit). That war has never been fought.”

Aberhart had learned from his mistakes during his first years in office and was ready, after World War II, to take up the fight again, but he unfortunately died in May of 1943. His successor, Ernest Manning, soon made it clear that he was not prepared to take up that fight and finally declared, in 1947, that his government would no longer do anything to implement Social Credit in Alberta. Incidentally, after retiring from politics, Ernest Manning became director of a bank.

So those who say that “Social Credit is that funny money scheme tried in Alberta, where it failed”, are dead wrong. Social Credit did not fail in Alberta, for the simple reason that it was never tried: all the attempts to implement Social Credit policies were opposed and defeated by a centralized power. As Douglas said, if Social Credit was absurd and worthless as an effective answer to the Great Depression, the best way to have this demonstrated would have been to allow the Government of Alberta to go ahead with a Social Credit policy. The credit monopolists feared that even a partial implementation of Social Credit would prove so successful that every effort had to be made to prevent this from taking place.

We firmly believe that the Social Credit principles, once implemented, would be a very efficient way to eliminate poverty. For the first time in history, absolute economic security, without restrictive conditions, would be guaranteed to each and every individual. So, dear reader, go ahead and study the following pages. You will find them most enlightening. Our hope is that this study will lead you to take action in making the Social Credit solution known to your fellow countrymen. Let us create a public pressure strong enough to get our governments to issue their own money, debt free, and to implement Douglas’s Social Credit principles.

The editors

Rougemont, March 1, 1996

Chapter 1 — A Few Principles

Man is a person

Man is a person. He is not a mere animal.

All people live in society. The more perfect people are, the more life in society is perfect. The society of angels is more perfect than human society. As for the three Divine Persons, They live in an infinitely intimate society, however, without merging into one.

Moreover, this Divine society is proposed to man as a model: “That they all may be one, as you, Father, in me, and I in you.” (John 17:21.)

Since men are human persons, they also live in society. Association responds to a need of man’s nature.

Man is a social being

Life in society responds to man’s nature for two reasons:

- Because the human being is a universe, in God’s image, and receives from the model, of whom he is the image, the tendency to give of himself, to communicate the wealth which he possesses;

- Because he is also a universe of indigence, in the temporal as well as in the spiritual world. The human being needs other human beings to come out of his indigence. He needs others physically for his conception, birth, growth. He needs others intellectually, too: without an acquired education, what intellectual level would a being who is born ignorant achieve?

We will not speak here of his spiritual indigence, nor of the need he has for the society called the Church.

In our studies, we will restrict ourselves to the temporal order, without, however, losing sight of the subordination of the temporal order to the spiritual order, because both the temporal and the spiritual orders concern this same man, and because the final end of this man takes precedence over all intermediary ends.

The common good

Any association exists for a goal. The goal of an association is a certain common good, which varies with the type of association, but it is always the good of each and every one of the members in the association.

It is precisely because it is the good of each and every one that it is a common good. It is not the particular good of only one of its members, nor of a section, that is sought by the association, but the good of each and every one of its members.

Three people join together for an enterprise. Peter contributes his muscle power; John, his initiative and experience; Matthew, his money capital. The common good is the success of the enterprise. But this success of the enterprise is not sought only for the good of Peter, nor only for the good of John, nor only for the good of Matthew. If one of the three is excluded from the benefits of the enterprise, he will not join.

The three form an association to achieve, for all and each of the three, a result that each of the three wants, but that none of the three can really derive alone. The money by itself would not give very much to Matthew; the arms by themselves would bring very little to Peter; the mind by itself would not be sufficient for John. But when the three combine their resources, the enterprise succeeds, and each one benefits from it. All three do not necessarily benefit to the same degree, but each of the three derives more than if he were alone.

Any association that frustrates its associates, or a part of its associates, weakens its bond. The associates are inclined to dissociate. When, in a big society, the marks of discontent become more pronounced, it is precisely because greater and greater numbers of associates are deprived more and more of their share of the common good. At such a time, legislators, if they are wise, seek and take the means to make each and everyone of the members participants in the common good. Trying to checkmate discontent by inflicting punishments on its victims is a very inadequate way of making it disappear.

Besides, since human associations are made of men, thus of people, thus of free intelligent beings, the common good of these associations has certainly got to be in keeping with the spreading out of intelligence and freedom. Otherwise, it is no longer a common good; it is no longer the good, through the association, of each and every one of the free intelligent beingss who compose the association

Ends and means

One must distinguish between ends and means, and especially subordinate the means to the end, and not the end to the means.

The end is the goal aimed at, the objective pursued. The means is the processes, the methods, the acts used to achieve the end.

I want to manufacture a table. My end is the manufacturing of the table. I get planks, I measure, I saw, I plane, I adjust, I nail the wood: so many movements, actions, which are the means used to manufacture the table.

It is the end that I have in sight, the manufacturing of the table, which determines my movements, the use of tools, etc. The end controls the means. The end exists first in my mind, even if the means have to be set to work before achieving this end. The end exists before the means, but it is reached once the means are used.

This seems elementary. But it often happens, in the running of public affairs, that one mistakes the means for the end, and one is all amazed when chaos results. (Editor’s note: This reminds us of what Pope John Paul II said before the General Assembly of the United Nations in New York, on October 2, 1979: “I ask you, ladies and gentlemen, to excuse me for speaking of questions that are certainly self-evident for you. But it does not seem pointless to speak of them, since the most frequent pitfall for human activities is the possibility of losing sight, while performing them, of the clearest truths, the most elementary principles.”)

Another example of this subject, on which we will return, is employment. So many legislators regard labour as an end of production, and are, by this, driven to demolish or paralyze all labour-saving devices! If they considered labour as a means of producing, they would be satisfied with the amount of labour necessary to achieve the sum of production sought.

Likewise, is the Government not a means to facilitate, for the Provinces, and for the Nation, the pursuit of the common good: therefore to serve, according to the common good, the people who compose the provincial association, the nation? In practice though, does one believe that the Government exists for the people, or the people for the Government?

One could say the same thing about systems. The systems were invented and established to serve man, not man created to serve systems. Then if a system is harmful to the mass of men, do we have to let the multitude suffer for the system, or alter the system so that it will serve the multitude?

Another matter which will be the subject of a long study in this volume: since money was established to facilitate production and distribution, does one have to limit production and distribution to money, or relate money to production and distribution?

Therefore one sees that the error of taking the ends for the means, the means for the ends, or of subordinating the ends to the means, is a stupid, very widespread error, which causes much disorder.

Hierarchy of ends

The end is therefore the objective, the goal sought. But there are far-off ends and more immediate ends, final ends, and intermediate ends.

I am in Montreal. A car company that I work for sends me to China to tie up commercial relations. I begin by taking the train from Montreal to Vancouver. There, I will embark upon a transoceanic liner which will take me to Hong Kong, where I will have recourse to public transportation for the rest of the tour.

As I climb aboard the train in Montreal, it is to go to Vancouver. To go to Vancouver is not the ultimate end of my journey, but it is the end of my journey by railroad.

To reach Vancouver is therefore an intermediate end. It is only an arranged means to the ultimate end of my journey. But, if it is only a means to the far-distant end, it is, in any case, an end as far as the journey by railroad is concerned. And if this intermediate end is not carried out, the ultimate end — tying up commercial relations in China — will not be reached.

The intermediate ends have a determined field. I must not ask the railroad to take me to Hong Kong. Neither must I ask the transoceanic liner to carry me from Montreal to Vancouver.

Besides, I must focus all intermediate ends on the ultimate end. If I take the railroad to Quebec City, I will undoubtedly be able to carry out this special end to perfection: reach Quebec City. But this will certainly not take me to my ultimate end: to tie up commercial relations in China.

You will see shortly the reason for all these elementary distinctions. They seem very simple in the present case: the business trip to China. One is often unaware of them, and one falls into a mess when one comes to the ends of economics.

Chapter 2 — Economics

When one talks about economy, one has a tendency to think of thrift, of savings. Have we not often been told: “Save your money, save your strength.”? We are clearly advised: “Save; do not spend.”

Nevertheless, we are also faced with the reflection: “Here is an economy which is not economical!” Thus, without being trained to the subtleties of the dictionary, people already grant a broader sense to the word economy.

For example, do not little girls of fourth-year primary school already study domestic economy? Going from domestic economy to political economy is nothing more than a question of extension.

The word economy is derived from two Greek roots: Oikia, house; nomos, rule.

The economy is therefore about the good regulation of a house, of order in the use of the goods of the house.

We may define domestic economy as good management of domestic affairs, and political economy as good management in the affairs of the large communal home, the nation.

But why “good management”? When can the management of the affairs of the small or large home, the family or the nation, be called good? It can be so called when it reaches its end.

A thing is good when it attains the results for which it was instituted.

The end of economics

Man engages in different activities and pursues different ends, in different orders, in different domains.

There is, for example, man’s moral activities, which concern his progress towards his final end.

Cultural activities influence the development of his intellect, the ornamentation of his intellect, and the formation of his character.

In participating in the general well-being of society, man engages in social activities.

Economic activities deal with temporal wealth. In his economic activities, man seeks the satisfaction of his temporal needs.

The goal, the end of economic activities, is therefore the use of earthly goods to satisfy man’s temporal needs. And economics reaches its end when earthly goods serve human needs.

The temporal needs of man are those which accompany him from the cradle to the grave. There are some which are essential, others which are not as vital.

Hunger, thirst, bad weather, weariness, illness, ignorance, create for man the need to eat, drink, clothe himself, find a shelter, warm himself, freshen himself, rest, to take care of his health, and to educate himself.

These are all human needs.

Food, drink, clothing, shelter, wood, coal, water, bed, remedies, the school teacher’s teaching books — these are all factors that must be present to fulfill these needs.

To join goods to needs — this is the goal, the end of economic life.

If it does this, economic life reaches its end. If it does not do this, or does it badly or incompletely, economic life fails its end or only reaches it imperfectly.

The goal is to join goods to needs, not only just to have them close together.

In straight terms, one could therefore say that economics is good, that it reaches its end, when it is sufficiently well-regulated for food to enter the hungry stomach, for clothes to cover the body, for shoes to cover naked feet, for a good fire to warm the house in winter, for the sick to receive the doctor’s visit, for teachers and students to meet.

This is the domain of economics. It is a very temporal domain. Economics has an end of its own: to satisfy men’s needs. The fact of eating when one is hungry is not the final end of man; no, it is only a means to aim better towards his final end.

But if economics is only a means to the final end, if it is only an intermediate end in the general order, it is nevertheless a distinctive end for economics itself.

And when economics reaches this distinctive end, when it allows goods to join needs, it is perfect. Let us not ask more of it. But let us ask this of it. It is the goal of economics to achieve this perfect end.

Morality and economics

Let us not ask of economics to reach a moral end, nor of morality to reach an economic end. This would be as disorderly as to attempt to go from Montreal to Vancouver in the transoceanic liner, or from New York to Le Havre, France, by railroad.

A starving man will not appease his hunger by reciting his Rosary, but by eating food. This is in order. It is the Creator who wanted it this way, and He turns from it only by departing from the established order, through a miracle. He alone has the right to break this order. To satiate man’s hunger, it is economics therefore that must intervene, not morality.

And similarly, a man who has a sullied conscience cannot purify it by eating a good meal, or by consuming copious libations. What he needs is the confessional.

It is religion’s place to intervene; it is a moral activity, not an economic activity.

There is no doubt that morality must accompany all of man’s actions, even in the domain of economics. But morality does not replace economics. It guides in the choice of objectives, and it watches over the legitimacy of the means, but it does not carry out what economics must carry out.

So when economics does not reach its end, when things stay in the stores or are not produced, and needs continue to be present in the homes, let us look for the cause in the economic order.

Let us blame of course those who disorganize the economic order, or those who, having the mission to govern it, leave it in anarchy. By not fulfilling their duties, they are certainly morally responsible, and fall under the sanction of ethics.

In effect, if both things are truly distinct, it happens nevertheless that both concern the same man, and that if one is immolated, the other suffers from it. Man has the moral duty to make sure that the economic order, the social temporal order, reaches its proper end.

Also, although economics is responsible only for the satisfaction of man’s temporal needs, the importance of good economic practices has time and time again been stressed by those in charge of souls, because it normally takes a minimum of temporal goods to encourage the practice of virtue.

Pope Benedict XV wrote, “It is in the economic field that the salvation of souls is at stake.”

And Pius XI:

“It may be said with all truth that nowadays the conditions of social and economic life are such that vast multitudes of men can only with great difficulty pay attention to that one thing necessary, namely their eternal salvation.” (Encyclical Letter Quadragesimo Anno, May 15, 1931.)

There is order everywhere — order in the hierarchy of the ends, order in the subordination of the means.

It is the same Pope who says in the same encyclical:

“This is the perfect order which the Church preaches, with intense earnestness, and which right reason demands: which places God as the first and supreme end of all created activity, and regards all created goods as mere instruments under God, to be used only in so far as they help towards the attainment of our supreme end.”

And immediately after, the Holy Father adds:

“Nor is it to be imagined that remunerative occupations are thereby belittled or deemed less consonant with human dignity. On the contrary, we are taught to recognize and reverence in them the manifest will of God the Creator, Who placed man upon earth to work it and use it in various ways in order to supply his needs.”

Man is put on earth by his Creator, and it is from the earth that he has the duty to wrest satisfaction of his nature’s needs. He does not have the right to shorten his life by doing without the goods that his Creator has put on earth for him.

To make the earth, the earthly goods, serve all of mankind’s temporal necessities is exactly the proper end of man’s economic activities: the adaptation of goods to needs.

Features of a human economy

Since men are beings who, by nature, live in society, a really human economy must be social. It must serve all members of society.

An economic organization that would allow the use of earthly goods to serve the needs of only a few, leaving the others in privation, would certainly not be social; it would therefore be inhuman.

If some members of society are practically banished from the economic benefits of society, and allowed, only grudgingly, what is strictly necessary to prevent them from rebelling against it, being treated rather like enemies to be pacified than like entitled members, the economic system is not human, but monstrous. This is an economic society of wolves.

In the jungle, in the struggle for life, the strong win and the weak disappear. Such a law is inadmissible among people, who are intelligent and social beings. A struggle for life among human beings can mean nothing but a collective struggle against common enemies: the wild beasts of forests, ignorance, the adverse elements. A really human economy must be based on the co-operation in life.

On the other hand, human beings, if they are social, are also free beings. And if a human economy must ensure the satisfaction of the essential needs of all men, it must do it without getting in the way of the person’s free blossoming.

The economy must not do violence either to sociability or to genuine freedom. A society of men is not a herd. An economy that sets conditions for the right to life on enrollment, is not human; it goes against man’s nature.

In the choice of the means to straighten a disordered economy, we will therefore choose the means that will respect man’s freedom.

Hierarchy

If the end of economics is a temporal end, it is therefore also a social end, to be reached socially. If it must satisfy man’s temporal needs, it must satisfy the temporal needs of ALL men.

This applies to all levels of social hierarchy, according to respective jurisdictions.

If it concerns the family, the domestic economy must seek the satisfaction of the needs of all members of the family.

Passing to the provincial economy, it must seek, within provincial jurisdiction, the satisfaction of the temporal needs of all the province’s inhabitants.

Likewise with the federal economy, it must satisfy human needs in what is within federal jurisdiction.

Encompassing the world economy, it is important that some connecting organism exists between nations, an organism respectful of the constituting parties’ autonomy to orient the world economy towards the satisfaction of the temporal needs of all men. The earth was created for all mankind.

But a good organization of society makes sure that the satisfaction of the temporal needs of ALL be effected as completely as possible within the circle of inferior levels, organisms in the more immediate contact with individuals.

So, instead of substituting itself for the family, to help the indigents, the State would be much wiser to legislate and organize the economic order in such a way that the family can itself respond, as perfectly as possible, to all of the needs of the members who compose it.

So, instead of substituting itself for the province, under the pretext that the provincial treasuries are broken and incapable of providing for immediate needs, the Federal Government would be much more in order if the provinces had financial means in keeping with their real wealth.

This is the Social Credit philosophy. It is, at the same time, truly more democratic.

Social Credit decentralizes the financial system. Centralization, State control, are the negation of democracy.

The social and very human end of the economic organism is summed up in this sentence of Quadragesimo Anno:

“Only will the economic and social organism be soundly established and attain its end, when it secures for all and each those goods which the wealth and resources of nature, technical achievement, and the social organization of economic affairs can give.”

ALL and EACH must be secured with all the goods that nature and industry can provide.

The end of economics is therefore the satisfaction of ALL of the consumers’ needs. The end is consumption; production is only a means.

To make economics stop at production is to cripple it.

To request from it the satisfaction of the needs of only a portion of society, when goods glut warehouses, is unreasonable and inhuman.

To abandon economics to hazard, to conflicting forces, is to capitulate shamefully, and to deliver the people to the teeth of the strongest.

Chapter 3 — The Consumers

The end of every economic activity is therefore the satisfaction of man’s needs. When he satisfies his needs, man fulfills the function of consumer.

The man who is hungry, eats; he consumes food. If he is cold, he clothes or warms himself; he consumes clothing or combustibles.

In an order where the end governs the means, it is man as consumer who is in charge of all of the economy. And since every man is a consumer, it is every man who contributes to orienting the production and distribution of goods.

It is for man, the consumer, that every economic activity exists. Man, as a consumer, must therefore organize production himself. It is he, the consumer, who must give his orders to the producers.

A really human economy is social, as we said; it must satisfy ALL men. So ALL and EACH must be able to give their orders to the production of goods — at least to satisfy their basic needs, as long as production is in a position to respond to these orders.

The needs of consumers — who can express them appropriately, if not the consumers themselves? This man, this woman, here in this apartment, over there at the door of their house, somewhere else in town, in the countryside, wherever they may be, whoever they may be — who can know their needs better than they themselves?

It is each consumer who knows his own needs. Therefore it is from each consumer that productive capacities must get orders. In a system really organized at satisfying the needs of consumers — of all consumers — all the consumers must have the means of expressing their needs, of ordering goods that answer these needs.

Production is unjustified in taking its orders from other sources than the consumers’ needs. This is nevertheless what happens when a firm puts pressure upon the consumers to push them to buying things for which they do not in the least feel a need. Then production takes its orders, not from the consumers, but from the search for profits.

One admits that irrational consumers, animals, men who do not have the use of their faculties or the sense of their needs, require outside intervention to dictate what they should get. But rational beings can determine their own needs.

Consumers must therefore be able to freely order useful goods for the satisfaction of their normal needs. Whatever may be the nature of the means adopted to express these orders, the orders must be able to come from the consumers as long as there are, on the one hand, unsatisfied normal needs, and, on the other hand, goods to satisfy these needs.

Chapter 4 — Goods

Do goods exist? Do they exist in sufficient quantity to satisfy all of the consumers’ basic needs?

Mankind has gone through periods of food shortage; famines covered big countries, and one lacked the appropriate means of transportation to bring to these countries the wealth from other sections of the planet.

It is no longer the case today. There is an overabundance of everything. It is abundance — no longer scarcity — that creates the problem.

It is not at all necessary to go into detail to demonstrate this fact. It is not in the least bit necessary to quote cases of voluntary destruction on a large scale “to stabilize markets”, by making stocks disappear.

The example of two world wars sufficiently proves the point.

From 1914 to 1918, and from 1939 to 1945, millions of human beings, in the prime of life — the ones most capable of producing — were rerouted from the production of useful things, and were employed at destruction. Industries, powerful machines were subjected to the same fate. And in spite of that, mankind still had in front of itself the necessities of life.

Famines are now nothing more than an artificial scarcity, wanted by some men. It takes minefields, submarines, torpedoes, blockades organized by force, to prevent abundance from overflowing to all the countries.

When one considers postwar problems, one never wonders where one will find wheat for the next day, or materials and workers. It is a different matter altogether, which bewilders statesmen and sociologists: What will they do with all these arms, machines, producing inventions, that the end of the war puts back into availability?

If, between both wars, all homes did not live in affluence, it was certainly not due to a lack of goods or the inability to produce. It was solely because the consumers did not have the means to order the goods that were produced.

Active production was far from being oriented in accordance with the real needs of the country’s men and women. It was production calculated mostly to make a profit, goods of no use for the ordinary man and woman, goods that were, in certain cases, even harmful.

A multitude of parasitic occupations, agencies, advertising campaigns — of which the existence is due to the incapacity of the consumers to express effectively their wishes — could have been employed usefully to serve consumers capable of expressing their wishes.

Without leaving our country, we can truly affirm that there exist no obstacles of material or technical order to satisfy the legitimate needs of ALL consumers.

Two kinds of goods

It is useful, in order to understand several price and purchasing-power problems, to distinguish between two kinds of goods.

On the one hand, there are goods which serve to support or embellish life. These goods are offered directly to the consumers for their use, and that is why they are called consumer goods.

Food, clothing, fuel, foodstuffs that one finds on the market, the doctor’s services, are consumer goods.

On the other hand, there are goods which are not put up for sale to the public, which are kept by producers precisely to produce consumer goods. Thus, a factory is not a consumer good. It is nevertheless a good, since it serves to produce consumer goods. The machines to make books, to manufacture shoes or clothing, to carry merchandise, fall in the same category as the factory.

These factories, machines, means of transportation, the goods that we do not buy, but which serve to produce other goods, are called capital goods. They are in fact the producers’ real capital. A farm is a capital good. It is the farmer’s capital.

Capital goods serve in production. We use the term “capital goods” and not “producer goods” in order to minimize confusion, because these goods include items which do not serve directly in production. Examples of these are roads, public buildings, and armaments.

To clarify this distinction between consumer goods and capital goods, as well as to show what is the use of this distinction, let us give an example of the different ways in which these two kinds of goods behave in relation to the consumers’ standard of living, at least under the present system.

One knows that to buy the products which are on the market, one must have money. Money is obtained mostly through wages and salaries. Wages and salaries are distributed to employees, whether they work to produce capital goods or consumer goods.

A man produces salable goods, let us say, shoes. With his wages, he can buy shoes, but never all the shoes that he makes. Another man works in an arms factory. With his wages, he buys neither shells nor machine guns, but salable goods, such as shoes. The two-combined wages can buy more of the production of the first wage-earner.

This means that the wages obtained for the production of capital goods, added to the wages obtained for the production of consumer goods, allow consumer goods — the only ones put up for sale —to be sold more easily.

It is the reason why industrial developments, which bring about new construction, or wars, which bring about the manufacture of armaments, create a kind of prosperity by allowing people to buy goods that they otherwise could not buy, because of the lack of money. This is why one says that when things are going well in the construction business, everything goes well. Whence comes this reflection which could appear cynical but which nevertheless expresses a factual trend: A good war would bring back prosperity (through employment).

For this reason, war is much more effective than construction. For example, if one talks about an ordinary industrial development, like a factory, once finished, it throws on the market goods which must recover the expenses of the factory. The problem of the lack of purchasing power then becomes more acute. War and arms factories put no products on the market; they even destroy or restrict the production of useful things by mobilizing manpower and machines while continuing to distribute wages and salaries to those who work at nothing but destruction.

Chapter 5 — Specialization — The Machine

As production progresses, the producer specializes. This specialization is itself a factor for a greater total production, requiring however less effort from each specialist.

For a long time now, some men have been cultivating the earth, some have been manufacturing materials, others worked at transportation, and others engaged in various kinds of services. But specialization increases, even on farms, and above all, in industry. Some workers make no more than a part, always the same part, of the finished product.

As far as output is concerned, this division of labour is certainly worthwhile, but it requires, for the satisfaction of the consumers’ needs, much more recourse to trade. Parallel to the development of the division of labour, of specialization, we must therefore have a flexible development in the trade mechanism.

The division of labour has furthered the invention of machines. In fact, the more the division, the more it is uniformly repeated, the more automatic becomes the movement of the worker who executes his very small part in the whole production process. That is tantamount to replacing human labour by machines.

The introduction of the machine contributes to increasing production, while reducing man’s work. The division of labour and the introduction of the machine are in perfect harmony with the determining principle of economic life in the field of production: the maximum effect with the minimum effort. But this division of labour and the introduction of the machine pose problems, which one has not yet been able to resolve.

If the division of labour has resulted in abridging, almost doing away with, the time necessary at apprenticeship, it has also, negatively, transformed labour into real toil. How boring and mind-destroying it must be to repeat the same movement, the same gesture, hour after hour, day after day, without having the satisfaction of thinking, devising, applying one’s mind! This is now the case in many occupations. Man’s creative faculties enter less and less into the worker’s daily labour; he becomes hardly more than a robot, a precursor to the steel machine.

One remedy would be to reduce working hours to the bare essentials, to provide leisure to this worker so he will be able to exercise his faculties to his liking, and become a thinking man again. Another remedy is to hasten the installation of the machine which will do, in the worker’s place, the repetitive movement which is already, strictly speaking, no longer a human task.

But with the present economic regulations, which require personal participation in production to get claims to production, one can imagine what happens when the worker is freed from work. Leisure is called unemployment, and the man thus released is a down-and-out.

Some people say that machines do not replace manpower in a lasting way, because new occupations, created by new needs, offer a new outlet to the unemployed, at least until the time when the machine drives them out again one day. Nevertheless, these disruptions, these continual expropriations of the worker’s labour, disorganize his life more and more, banish all security, prevent him from building for the future, and force the multiplication of State interventions.

Therefore, must one agree with those who oppose the introduction of almost all new machines? Not at all. But the system of goods distribution must be adapted. Since machines increase the quantity of goods instead of decreasing them, mechanical production ought to increase production in the homes, even if man’s personal labour in production decreases. This ought to be done without collisions and upheavals. It is possible, provided one dissociates – to the required degree – claims on production from a personal contribution in production.

This, you will see further, is what Social Credit can do, by introducing into distribution the system of dividends to EACH and EVERYONE, to the extent that the wage-earners cannot buy all of the available goods, because of their lack of purchasing power.

With production being more and more specialized and mechanized, each producer, man or machine, supplies, in line with the job, a more and more considerable quantity of goods that they, men or machines, do not themselves consume. Now, all that a producer supplies, over and above his personal needs, is for the use of the rest of the community. Thus, all of a farmer’s production, over and above his family’s needs, is necessarily for the use of the rest of the community. All of a blacksmith’s production, save what is for his family’s use, is destined only for the use of others in the community.

Not that the farmer or the blacksmith must give to his neighbours or to the State what his family does not use. What his family does not consume is produced only for the consumption of the rest of the community, and in some way must go to the rest of the community.

As for the machines, they consume nothing of what they produce. So their immense production enlarges these surpluses that, in some way, must reach the consumers for production to carry out its end.

One can set any appropriate rules so that no worker will be injured. It will be necessary however that, in some way, the consumers are able to draw upon this plentiful production, which exceeds the particular needs of the producers who have brought it into being. And the more plentiful this non-absorbed production is by its makers, the larger its flow must be, and the more generous must be the claim which gives right to it.

Chapter 6 — Poverty amidst Plenty

The abundance of goods introduced into the world, since man discovered the means of transforming energy and harnessing the forces of nature to his service, ought to be reflected in economic security for all — which means, at the very least, modest material comfort in every home, in an era of good, joyful, and peaceful social relations among individuals and nations.

Unfortunately, the picture that meets the eye in all the civilized countries of the world is quite different. In front of an abundance of goods that pile up, except when they are destroyed in wartime, destitution takes place.

Elevators and warehouses are full to overflowing; shop windows, newspapers, radio and TV announce everywhere a wide range of products, while people in their homes have to do without food, and use their rags and old furniture longer than ordinary.

“What percentage of our population is merely existing rather than enjoying the use of available and sufficient wealth to live in reasonable comfort? At least three-fourths of our population.” (Rev. Charles E. Coughlin, Money, page 26.)

But quotations are hardly necessary. Most readers have only to examine their personal situations and that of their neighbours. So who, today, is ensured of a reasonable comfort for tomorrow?

No one doubts that tomorrow Canada can continue to supply in plenty what is needed in terms of food, clothing, and housing. But how many people are assured of having a sufficient share for themselves and their families tomorrow, the day after tomorrow, next year?

The number of unemployed and laid-off workers should, logically, show an overabundance of goods, and that consumption has reached saturation point. This number means, above all, sufferings, destitution, and desperation.

The goods are there in front of human needs. So why is it that these goods do not fill these existing needs? What prevents the economy from reaching its end?

Why is it that consumers, who have so many unsatisfied needs, cannot use these goods made for them?

The existence of widespread poverty, in front of so much production and unused production capacity, is a terrible accusation against the distributive system.

Never has supply been so great. In front of this supply, is there actually no demand?

Demand exists. But the claim on supply, the right to have it, is wanting; this claim is money.

Real demand, effective demand

One should make a distinction between real demand and effective demand.

Real demand ensues from real needs. As long as there are people who are hungry, there exists a real demand for food. As long as there are people without proper shelter, there is a real demand for housing. As long as there are sick people, there is a real demand for medicine and medical care.

But this real demand becomes effective only if it presents the claim to production: money.

Effective demand exists only where money is united to needs.

Under the present economic system, one usually notices a lot of real demands without the claims that would make these demands effective. The producers, forced to recover their expenses, look for places where there is still some money left, and then do everything possible to create a demand. This is to sell under pressure, which no longer answers the needs of the consumers, but the needs of the producers.

This is a reversal of the economic order. The consumers become exploited victims, and no longer the masters to serve.

The humane solution would be to put money where the needs are, thus making the real demand effective; and not to create artificial needs where the real demand does not exist.

Major Douglas points out that to reconcile the real demand and the capacity to pay, the will-to-power will have to be defeated by the will-to-freedom, and that this reconciliation involves a modification of the distributive system. (See Economic Democracy, page 90.)

He adds, with a sound conception of the end of economics:

“Now if there is any sanity left in the world at all, it should be obvious that the real demand is the proper objective of production, and that it must be met from the bottom upwards, that is to say, there must be first a production of necessaries sufficient to meet universal requirements; and, secondly, an economic system must be devised to ensure their practically automatic and universal distribution; this having been achieved it may be followed to whatever extent may prove desirable by the manufacture of articles having a more limited range of usefulness. All financial questions are quite beside the point; if finance cannot meet this simple proposition then finance fails, and will be replaced.”

Since production exists to satisfy the needs of the consumers, and since, according to regulations generally accepted, the consumer must present money to be able to draw upon production, the money in the hands of the consumers must be in keeping with their needs, combined with the country’s production capacity. If this is not so, money works against the consumers, therefore against man. In this case, a change is essential.

It is because the present monetary system hinders the satisfaction of the consumers’ needs, that certain people propose the abolition of money. According to them, the State would then seize all of the production that is not consumed by its authors, and would itself distribute it to all the members of the community.

This is the Communist solution, which nobody wants in our country. Yet, one cannot approve of the immobilization of goods and production in front of urgent needs.

We will not even consider the dictatorial solution, in which it is no longer the consumers who express their needs: A superman dictates to all what they should have, and to production what it should do. In such a system, guns may well be produced at the expense of bread.

There is another solution — the solution which, in putting money in the hands of the consumers, of ALL consumers, gives them ALL the right to choose products. Then the consumers really orient production. It is the Social Credit solution. It brought a sociologist to write:

“And if you want neither Socialism nor Communism, bring Social Credit in array against them. It will be in your hands a powerful weapon with which to fight these enemies.” (Rev. Georges-Henri Lévesque, O.P., in Social Credit and Catholicism.)

But one must first study this money question, to understand whence the shortcomings of the monetary system, and how to make the system work and fulfill its role.

Chapter 7 — The Symbol and the Thing

Better than anyone else, the Social Credit school knows how to distinguish between wealth and money. If, in its studies, it gives so much importance to money, it is because money today is necessary to have access to wealth.

In normal times, when war does not introduce wholesale destruction, the civilized world abounds in wealth. The storekeepers then never complain of not being able to find what is needed to replace sold stocks. Warehouses are full to bursting. The hands of able-bodied men are more numerously offered than can be employed.

The civilized countries have so many products that they search everywhere abroad to sell them. By all means, they favour exportation, and they bar the road to importation, so as not to be glutted with products.

It is Canada’s situation. Canada is a country overflowing with wealth, and capable of producing even more.

But, what is the use of saying to Canadian men and women that their country is rich, that it exports a great many products, that it is the third- or fourth-ranking country in the world for exportation? What goes out of the country does not go into Canadian homes. What stays in the stores does not appear on the tables of the Canadians.

A mother does not feed her children or provide them with garments by going window-shopping, by reading product advertisements in newspapers, by listening to beautiful product descriptions on the radio, by listening to sales talk from countless sales representatives of all kinds.

It is the claim on these products that is lacking. One cannot steal them. To get them, one must pay; one must have money.

There are a lot of good things in Canada, but when the claim on these things is absent from the Canadians’ hands, when people do not have money, what is the purpose of the display of all this wealth?

This does not mean that money itself is wealth. Money is not an earthly good capable of satisfying temporal needs.

You cannot keep yourself alive by eating money. To get dressed, you cannot sew dollar notes together to make a dress or a pair of stockings. You cannot rest by lying down on money. You cannot cure an illness by putting money on the seat of the illness. You cannot educate yourself by crowning your head with money.

No, money is not real wealth. Real wealth is the useful things which satisfy human needs. Bread, meat, fish, cotton, wood, coal, a car on a good road, the doctor’s visit to a sick person, the teacher’s science — this is real wealth.

But, in our modern world, each individual does not produce all the things he needs. People must buy from one another. Money is the symbol or token that one gets in return for something sold; it is the symbol that must be presented to get something offered by another.

The symbol ought to reflect the thing

Wealth is the thing; money is the symbol of that thing. Logically, the symbol ought to reflect the thing.

If a country has a lot of things available for sale, there must be a lot of money available to dispose of them. The more people and goods, the more money in circulation is required, or else everything stops.

It is precisely this balance which is generally lacking. We have at our disposal almost as great a quantity of goods as we could possibly wish for, thanks to applied science, to new discoveries, and to the perfecting of machinery. We even have people reduced to forced unemployment, who represent a potential source of goods. We have loads of useless, even harmful, occupations. We have a great deal of activities, of which the sole end is destruction.

Money was created for the purpose of keeping goods moving, of selling goods. Why then does it not always find its way into the hands of the consumers in the same ratio as goods flow from the production line?

Why? Because goods come from one source, and money comes from another source. The first source — production — works well, but the latter — money — does not work properly.

A source of goods is the natural resources with which Providence has favoured the planet; other sources are applied science and the work of producers. All of these supply products in abundance.

The source of money is elsewhere. Money comes neither from Providence, nor from science, nor from the farmer’s furrows, nor from the fisherman’s net, nor from the blows of the woodcutter’s axe, nor from the workman’s skill.

And the source of money does not run parallel to the source of products, since money was lacking before World War II, in front of an abundance of goods available for sale, and since money came during the war, in front of the stores lacking in products.

Products come through production, and they disappear through consumption. Money too comes and disappears, since it is plentiful at times, scarce at other times. Money comes into being and dies.

Chapter 8 — The Birth and Death of Money

A mysterious birth

Where do potatoes come from? — From the farmer’s field. Where are little calves born?— In the cowshed. Where do plums come from? — From the plum tree.

Everybody knows that. But now ask the same question about money:

Where does money come from? Where is born the paper dollar that I have in my pocket? Who gave birth to it, for what reason, and in what circumstances?

Where were the millions and millions of dollars born with which the Government financed the war, the Government which had noticed for the previous ten years that there were not enough dollars in the country to just finance ordinary public works?

Then, where do dollars go to when one cannot see them any more? Where did the dollars go during the 1930-1940 Depression, those dollars which had financed the country so well from 1925 to 1929?

Where are dollars born, and where do they die?

Ask people these questions, and tell me how many are able to answer you.

Neither God nor the temperature creates dollars. And yet dollars are not created by themselves! Who creates them? Who knew how many to create to pay for the war? And why did they, who had created the dollars to carry on the war, not create any beforehand to settle the Depression?

Two kinds of money

In order to clearly understand where money begins and where it ends, one must distinguish between two kinds of money, equally good: coins and paper money, and bookkeeping money.

Coins and paper money is only pocket money, which ordinary people use every day.

The big industrialists, the big retailers, more regularly use bookkeeping money. To make use of bookkeeping money, one must simply have a bank account.

Let us suppose that I have a bank account with $2,000 to my credit. I buy an electric washing machine at Sears. It costs $600. I pay for it with a $600 cheque on my bank account. What will happen?

I will receive my washing machine. The Sears firm will deposit my cheque at its own bank. The banker will raise the Sears firm’s credit by $600. Sears’ bank will then send the cheque to my bank. The banker will decrease the credit of my account by $600. And that is all. Not one dollar will have left a pocket or a drawer. An account will have increased — the retailer’s; another one will have decreased — mine. I have paid with bookkeeping money.

Bookkeeping money is the credits in bank accounts.

This kind of money accounts for 90 percent of all commercial transactions. It is the main kind of money in civilized countries, like ours.

Furthermore, it is when bookkeeping money increases, that pocket money increases, and it is when bookkeeping money decreases, that pocket money decreases. When ten dollars of bookkeeping money goes into circulation, one dollar of pocket money (coins or paper money) enters into circulation. When ten dollars of bookkeeping money disappears from circulation, one dollar of pocket money disappears from circulation. It is at least the current ratio.

Bookkeeping money is in control. It is its quantity that determines the quantity of the other kind of money (cash).

Money begins in the banks

To find out where money originates and ends, one must find out where bookkeeping money originates and ends. Bookkeeping money, which controls everything, is a credit in a bank account.

Increasing credits in some bank accounts, while decreasing them in other accounts, is merely a transfer of bookkeeping money. If the credits correspond to metal or paper money deposited in the bank, it is a change from pocket money to bookkeeping money. But if the credits in bank accounts are increased without any decrease elsewhere, new bookkeeping money, which increases the total volume of money available, is generated.

When I save and then deposit $100 in the bank, the bank writes down $100 to my credit. This gives me $100 in bookkeeping money. But it is not new money; it is merely money that has passed from my pocket to the bank, or from the account of someone who has issued me a cheque to my own account. It is not the birth of new money; it is simply savings.

But, if instead of bringing my savings to the bank, I come to the bank to borrow a great deal of money, let us say $100,000, to enlarge my factory, what actually happens?

The bank manager has me sign some forms and pledges. Then he hands me a discount cheque that I deposit with the teller. The teller simply writes $100,000 to my credit. He records the same amount in my bankbook.

I leave the bank without carrying any cash on me, but I have added $100,000 of bookkeeping money to my credit, which I did not have upon entering. This allows me to pay, by cheques, up to an amount of $100,000 for machines, materials, and workers.

Moreover, no other account in the bank was decreased to accomplish this. Not a penny was moved, whether from a drawer, a pocket, or an account. I have $100,000 more, yet no one has a penny less.

This $100,000 did not exist an hour ago, and yet here it is entered into my credit, into my bank account.

Where then does this money come from? This is new money which did not exist when I walked into the bank, which was neither in the pocket, nor in the account, of anyone, and yet it now exists in my account.

The banker actually created $100,000 of new money in the form of credit, in the form of bookkeeping money, which is just as good as coins and paper money.

The banker is not afraid to do this. My cheques to payees will give them the right to draw money from the bank. But the banker knows very well that nine-tenths of these cheques will simply have the effect of decreasing the money in my account, and of increasing it in other people’s accounts. He knows very well that a ratio of bank reserves to deposits of 1/10 is enough for him to answer the requests of those who want pocket money. In other words, the banker knows very well that if he has $10,000 in cash reserves, he can lend $100,000 (ten times the sum) in bookkeeping money.

– Editor’s note: The preceding paragraph was written in 1946, and this ratio (a 10% cash reserve requirement) has changed since then. In 1967, the Canadian Bank Act allowed the chartered banks to create sixteen times (in bookkeeping money) the sum of their cash reserves. Beginning in 1980, the minimum reserve required in cash (bank notes and coins) was 5 per cent, which meant that the banker needed only one dollar out of twenty to answer the needs of those who wanted pocket money. The banker knew very well that if he had $10,000 in cash, he could lend twenty times the sum, or $200,000, in bookkeeping money.

In practice, the banks could lend out even more than that, since they could increase their cash reserves at will by simply purchasing bank notes from the central bank (the Bank of Canada) with the bookkeeping money they create out of thin air, with a pen. For example, it was established in 1982, before a parliamentary committee on banks’ profits, that in 1981, the Canadian chartered banks, as a whole, made loans 32 times in excess of their combined capital. A few banks even lent sums equal to 40 times their capital. Moreover, in 1990 in the U.S.A., the total deposits of commercial banks amounted to about $3,000 billion, and their reserves amounted to approximately $60 billion. This resulted in a ratio of deposits to bank reserves of about 50/1. U.S. banks held enough cash to pay off depositors at the rate of only about two cents on the dollar.

Subsection 457(1) of the most recent version of the Canadian Bank Act, enacted on December 13, 1991, states that, as of January, 1994, the primary reserve, in the form of cash, that a chartered bank has to maintain is nil, zero. So the banks are no longer limited by law in creating credit, or bookkeeping money. (And if all cash is eventually replaced by electronic money, with debit or microchip cards, as it is already planned by the banks, they won’t even be limited in practice to create money, which will then not be a piece of paper or an entry in a ledger, but simply bytes, units of information in a computer.)

The increase in the money supply

When it is the Government that borrows from the banks, the procedure is the same. The amounts are much greater, because the entire wealth of the country is involved. All the power to tax is then used as a pledge to the banker, in the form of debentures.

When the war broke out in 1939, the Government, which for the last ten years had been short of money, went to the banks to carry out a first loan of $200 million. The banks did not have any more money than they had had the day before. For the last ten years, the population had been lacking money. When one is lacking money, one hardly has any surplus to bring to the banks.

Nevertheless, the banks loaned $200 million to the Government. They wrote to the Government’s credit $200 million in bookkeeping money. And the young people, who had been wandering about aimlessly for years because there was no money, were called immediately by the Government, dressed from head to toe, lodged, fed, equipped, and transported to Europe to take part in the slaughter.

And this was seen in all the countries of the world. The world had suffered from unemployment for ten years, due to the scarcity of money. This same world was able to fight a very costly war, because the banks had created all the bookkeeping money that was needed to finance the war.

Canada’s banks thus created, during the war, at least 3 billion dollars of new money to finance the Canadian share of the universal butchery.

Money is easy to create, since all that is needed is the banker’s pen. And yet, before the war, due to the lack of money, the world did penance for ten years, and no government made an order to make use of the banker’s pen.

The death of money

But this bookkeeping money, created by the banks, is created under certain conditions. It must be brought back within a determined period of time, along with other money, in the form of interest.

Thus, one million dollars loaned at 5 percent for a period of twenty years, obliges the Government, which borrows this sum, to pay back 2 million dollars within twenty years — $1 million in principal and $1 million in interest.

As the Government does not create money, and as it cannot pump out from the public more money than was put into circulation, it is never able to bring back to the banker more money than the banker created. The more the Government tries to meet its obligations, the more it creates a scarcity of money in the country. It must even borrow other amounts to be able to pay indefinitely the interest on the principal thus created by the banks.

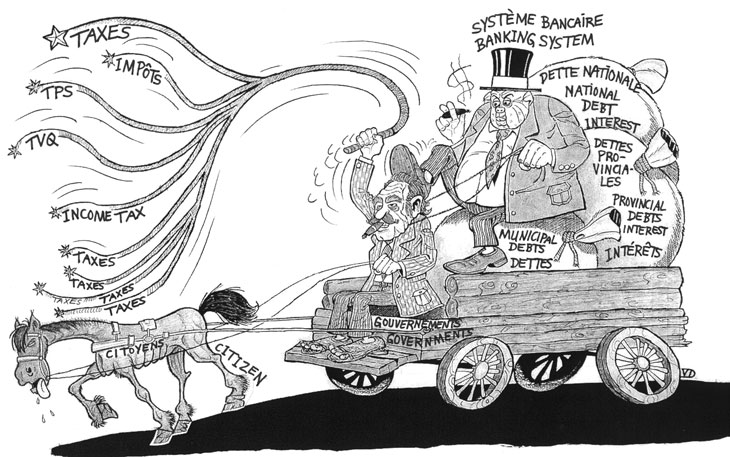

This is the reason why the public debt always increases, why interest on this debt is ever greater, and why taxes to pay the interest charges are more and more burdensome.

As for private individuals who thus borrow from the banks, they must either pay back with interest, or go bankrupt. If some succeed, it is by extracting from consumers, through the sale of products at raised prices, more money than they have put in. The success of some, in a system where money begins in the form of a debt, laden with interest, necessarily causes the bankruptcy of others.

Nine-tenths of the money that returns to the bank to repay loans enters the bank in the form of credit, and is simply cancelled; this money ceases to exist. The bank is both the cradle and the grave of money. It is both a factory that creates money and a slaughterhouse that cancels money.

When repayments are demanded faster than new loans are made, the slaughterhouse functions more rapidly than the factory. The result is a depression. This was how the 1930-1940 Depression originated.

When loans are more generous and more frequent than repayments, the factory runs more rapidly than the slaughterhouse, and money becomes plentiful. This is what happened during the war: money was more plentiful than the products.

It is quite obvious that the amount of money in circulation depends on the banks’ actions. And the banks’ actions do not depend at all on production or needs.

A pernicious dictatorship

In a world where one cannot live without money, one understands that a system which thus gives to private interests — the banks — the power to regulate the amount of money as they please, puts the world at the mercy of the makers and the destroyers of money.

Those who control money and credit have become the masters of our lives. No one dare breathe without their permission. This is what Pope Pius XI said.

A striking point must be emphasized:

It is production that gives value to money. A pile of money without corresponding products does not keep anyone alive, and is absolutely worthless. Thus, it is the farmers, the industrialists, the workers, the professionals, the organized citizenry, who make products, goods and services. But it is the bankers who create the money, based on these products. And the bankers appropriate this money, which draws its value from the products, and lend it to those who make the products.

Chapter 9 — The Monetary Defect

The situation amounts to this inconceivable thing: all the money in circulation comes only from the banks. Even coins and paper money come into circulation only if they are released by the banks.

But the banks put money into circulation only by lending it out at interest. This means that all money in circulation comes from the banks and must be returned to the banks some day, swelled with interest.

The banks remain the owners of the money. We are only the tenants, the borrowers. If some manage to hang on to their money for a long time and even permanently, other people are made incapable of fulfilling their commitments.

A multiplicity of personal and corporate bankruptcies, mortgages upon mortgages, and the continuous growth of the public debt, are the natural fruits of such a system.

Charging interest on money at birth, as it comes into existence, is illegitimate and absurd, antisocial, and contrary to good arithmetic. The monetary defect is therefore as much a technical defect as a social defect.

As our country grows, in production as well as in population, more money is a must. But it is impossible to get new money without contracting a debt, which collectively cannot be paid.

So we are left with the alternatives of either stopping growth or going into debt; of either plunging into mass unemployment or of having an unrepayable debt. And it is precisely this dilemma that is being debated in every country.

Aristotle, and later, Saint Thomas Aquinas, wrote that money does not produce offspring, does not breed more money. But the bankers bring money into existence, provided only that it breeds more money. Since neither governments nor the public create money, no one creates the offspring (the interest) claimed by the banker. Even legalized, this form of issue remains vicious and insulting.

Decline and degradation

This way of creating our country’s money, by putting governments and individuals in debt, establishes a real dictatorship over governments and individuals alike.

The sovereign government has become a signatory of debts owed to a small group of profiteers. A minister, who represents all of the population of the country, signs unrepayable debts. The banker, who represents a few shareholders who thirst after profits, manufactures our country’s money.

This is one striking aspect of the degeneration of power, of which Pope Pius XI spoke: governments have surrendered their noble functions, and have become the servants of private interests.

The Government, instead of guiding Canada, has become a mere tax collector, and the biggest item in government expenditures is precisely debt servicing: payment of the interest on the public debt.

Furthermore, legislation consists mainly in taxing the citizens, and erecting, everywhere, restrictions to freedom.

There are laws to make sure that the money creators are repaid. There are none to prevent human beings from dying in dire poverty.

Tight money develops a mentality of wolves in individuals. In front of plenty, everyone tries to get the too scarce symbols of the goods that give a right to a share in this plenty. Hence, frantic competition, patronage, denunciations, the tyranny of the “boss”, domestic strife, etc.

A handful of people preys on the others; the great mass of the people groan; many founder in the most degrading poverty.

Sick people remain without care, children are poorly or insufficiently nourished, talents go undeveloped, youths can neither find jobs nor start homes and families, farmers lose their farms, industrialists go bankrupt, families struggle with difficulties — all this without any other cause than the lack of money.

The banker’s pen imposes privations on the public and servitude on the governments.

Chapter 10 — Putting the Monetary System Right

Who must create money?

It is Saint Louis, King of France, who said: “The first duty of a king is to create money when it is lacking for the sound economic life of his subjects.”

It is not at all necessary or to be recommended that banks be abolished or nationalized. The banker is an expert in accounting and investment; he may well continue to receive and invest savings with profit, taking his equitable share of profits. But the creation of money is an act of sovereignty that should not be left in the hands of a bank. Sovereignty must be taken out of the hands of the banks, and returned to the nation.

Bookkeeping money is a good modern invention that should be retained. But instead of having these figures proceeding from a private pen, in the form of a debt, these figures, which serve as money, should come from the pen of the sovereign, in the form of money destined to serve the people.

Therefore nothing is to be turned upside down in the field of ownership or investment. There is no need to abolish the current money, to replace it with other kinds of money. The Government needs only, on behalf of society, to institute a system which adds enough of the same kind of money to the money that already exists, according to the country’s possibilities and needs.

To this end, the Government must establish a monetary body, a National Credit Office. The accountants of this Office, although appointed by the Government, would not take their orders from it. Neither would they dictate anything to the producers, nor to the consumers. Their function would consist simply in matching the mechanism for the issue and withdrawal of money with the rate at which wealth is produced and consumed by unrestrained producers and consumers. Somewhat like the judicial system: judges are appointed by the Government, but their judgments are based solely on the law and exposed facts, two things they neither authored nor instigated.

People must stop suffering from privations when there is everything needed in the country to bring comfort into every home. Money must be issued in accordance with the country’s production capacity and with the demand of the consumers for possible and useful goods.

Who owns the new money?